Our strategists summarise market performance and the outlook for next month.

Global equities advanced over the month, as robust earnings results and better than expected economic growth bolstered investor sentiment.

US stocks moved higher after the US Senate passed a budget vote that lawmakers expect will pave the way to a tax overhaul deemed critical to Republicans’ prospects in elections next year. The US economy grew by 3% in the third quarter, beating forecasts of a 2.5% expansion.

European Commission president Jean-Claude Juncker said that the UK would need to pay its “divorce bill” before discussions can proceed on trade and future relations between the UK and the European Union. Meanwhile, the International Monetary Fund singled Britain out as a “notable exception” to an improving global economic outlook – slashing the country’s long-term growth outlook.

The European Central Bank reduced its quantitative easing scheme to a monthly pace of €30 billion from January with the option of extending it beyond September 2018. That amount is down from the current €60 billion-a-month buying pace.

The UK economy expanded faster than anticipated over the third quarter, increasing the likelihood of an interest rate hike at the Bank of England’s next Monetary Policy Committee meeting.

Strategist’s Outlook

In terms of regions, valuations remain expensive in the US and as such, we still believe that other regions remain more attractive.

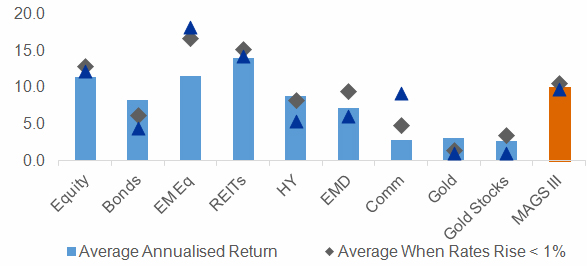

As expected, the Bank of England has increased interest rates by 0.25 percentage points to 0.5% - the first rate rise since 2007. We believe this rate hike will be moderately negative to the UK’s economic outlook, especially to the consumption and housing sectors, and this could become a headwind factor for UK equities.